Most consumers want to know where their money is going each month, instead of wondering where to get money now. A budget may help you feel more in control of your finances and make saving money for your objectives simpler. The goal is to find a method of tracking the money that works for you. The techniques below can help you create a budget.

Step 1: Determine Your Net Income

A great budget is built on your net income as its main component. That is your take-home pay—your total income or salary fewer tax deductions and employer-provided benefits like retirement plans and health insurance.

Focusing on your total compensation rather than your net income may lead to overspending since you will believe you have more money available than you really have. If you operate as a freelancer, gig worker, contractor, or are self-employed, maintain accurate records of your contracts and payments to help you handle irregular revenue.

Step 2: Keep Track of Your Expenditures

Once you’ve determined how much money is coming in, the next step is to determine where it’s going. Tracking and classifying your costs will help you figure out where you’re spending the most money and where you might be able to save the most.

Begin by making a list of your fixed costs. These include monthly costs such as rent or mortgage payments, utilities, and automobile payments. Next, make a list of your variable costs, which might vary from month to month, such as food, petrol, and entertainment.

This is an area where you may be able to save money. Credit cards and bank statements are excellent places to start since they often itemize or classify your monthly expenses. Record your daily expenditures using whatever you have available, whether it’s a pen and paper, an app on your smartphone, or budgeting spreadsheets or templates obtained online.

Step 3: Establish Attainable Objectives

Make a list of your short- and long-term financial objectives before you begin combing through the data you’ve collected. Short-term objectives should be completed within one to three years and may include things like putting up an emergency fund or paying off credit card debt.

Long-term objectives, like saving for retirement or your child’s education, might take decades to achieve. Remember that your objectives do not have to be etched in stone, but knowing what they are will help drive you to stay within your budget. For example, if you know you’re saving for a trip, it may be simpler to cut down on spending.

Step 4: Create a Strategy

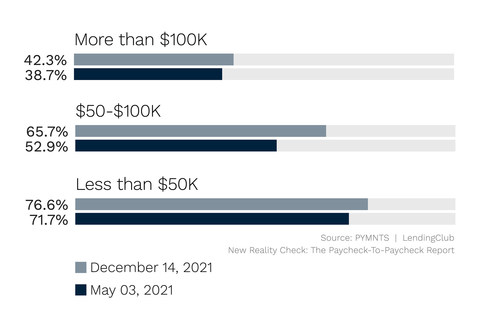

According to a recent study, about 59 percent of individuals in the United States acknowledged living paycheck to paycheck. This means that more than half of Americans are constantly worried about money, and one unexpected expense can cause serious financial hardship.

The survey also found that 78 percent of respondents had less than $1,000 in savings, and 34 percent had no savings at all. These numbers are sobering, but they’re not surprising. wages have been stagnant for years, while the cost of living has steadily risen. As a result, many people are struggling to make ends meet.

The good news is that there are steps that can be taken to improve the situation. For example, creating a budget and automating savings can help people get control of their finances and start building up a cushion against tough times.

Use the variable and fixed costs you accumulated to estimate how much you’ll spend in the following months. After that, compare it to your net income and priorities. Consider establishing clear (and reasonable) spending limitations for each area of cost.

You may wish to further divide your costs into items you must have and those you desire to have. For example, if you drive to work every day, fuel is considered a need. A monthly music membership, on the other hand, may be considered a wish. This distinction is significant when you’re searching for strategies to channel money toward your financial objectives.

Step 5: Outline Your Savings Objectives

If you’re going to save money, having a particular objective to strive toward will help you stay motivated. Consider what you want to achieve with your savings, both in the short and long term. For example, you may want to save money for a trip in the next six months, or you may want to save for a down payment on a house in the next year.

Consider what you want to do with your money, and then break it down into distinct, concrete stages. To keep motivated on your savings journey, set a deadline for each objective and measure your progress.

Step 6: Modify Your Expenditures to Keep Under Your Budget

You may make any required modifications now that you’ve recorded your income and expenditures so that you don’t overspend and have money to invest toward your objectives. Cuts should be made initially in the area of your “wants.”

Can you forego movie night in favor of seeing a movie at home? If you’ve already reduced your spending on desires, examine your expenditure on monthly payments. Close scrutiny reveals that a “need” may just be “hard to part with.”

If the figures still don’t add up, consider altering your fixed costs. Could you, for example, save more money by comparing vehicle and homeowners insurance rates? Such selections include significant trade-offs, so carefully consider your alternatives.

Remember that even tiny saves may build up to a significant amount of money. You may be shocked at how much money you can save by making little changes one at a time.

The primary purpose of making a budget is to help you keep your finances under control by tracking how much money you spend and where it goes. When you begin to deviate from your budget, it is typically due to overspending someplace.

But why is it so simple to overspend if you have a budget that informs you precisely how much you’ve meant to spend? There are many reasons why we overspend, and by understanding what causes it, you can help put a stop to it and keep your budget on track.

Step 7: Make Your Savings Plan Automated

It might be difficult to remember to save money at times. Saving automatically is a simple method to keep on track with your savings strategy. To create your emergency fund, set up automatic transfers from your checking account to your savings account.

To start saving for retirement, open an individual retirement account and set up automatic contributions every paycheck. Automating contributions into several accounts guarantees that you are saving rather than spending, and the power of compound interest may help your money increase consistently over time.

Step 8: Review Your Budget on a Frequent Basis

Once you’ve established your budget, it’s critical to check it and your expenditures on a regular basis to ensure you’re on track. Few aspects of your budget are fixed: you may receive a raise, your costs might alter, or you might attain a goal and wish to establish a new one. Whatever the cause, get into the practice of checking in with your budget on a regular basis by following the steps outlined above.